China imposes graphite export restrictions

Export restrictions on key anode materials highlight the dominance of China in the battery sector, and the case for localised supply chains

In October 2023, China’s Ministry of Commerce and the General Administration of Customs announced that effective December 2023, export permits would be imposed on key lithium-ion battery anode raw materials. The affected products were high purity synthetic graphite and its products, and natural flake graphite and its products including spherical and expanded graphite.

The export controls were imposed by China on the grounds of safeguarding domestic interests. They come following increased controls on export of advanced semiconductor chips to China by the US and investigation into Chinese electric vehicle (EV) subsidies by the EU. These restrictions have the potential to have far reaching consequences for materials required for the EV sector.

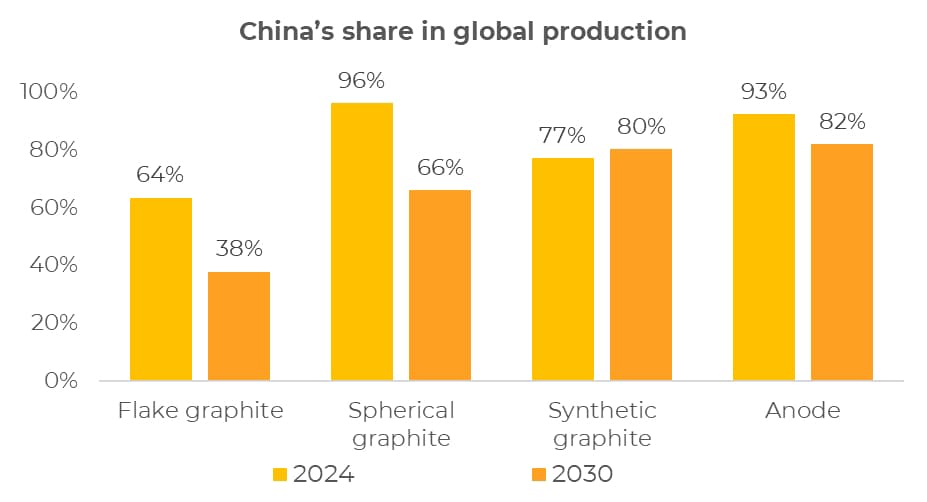

China boasts a dominant position in the global graphite industry. The country accounts for over 60% of flake graphite and nearly 80% of synthetic graphite production globally. The imbalance is more pronounced for value-added products such spherical graphite and anode active material where China controls more than 90% of global production.

Chinese anode manufacturers such as BTR, Shanshan and Putailai are suppliers for leading battery companies such as Panasonic, CATL and LG Energy solution underpinning the interdependency of the global battery supply chain. Export restrictions have highlighted the market influence China possesses and the need for the rest of the world to develop alternative and localised supply chains.

Source: Benchmark Forecasts

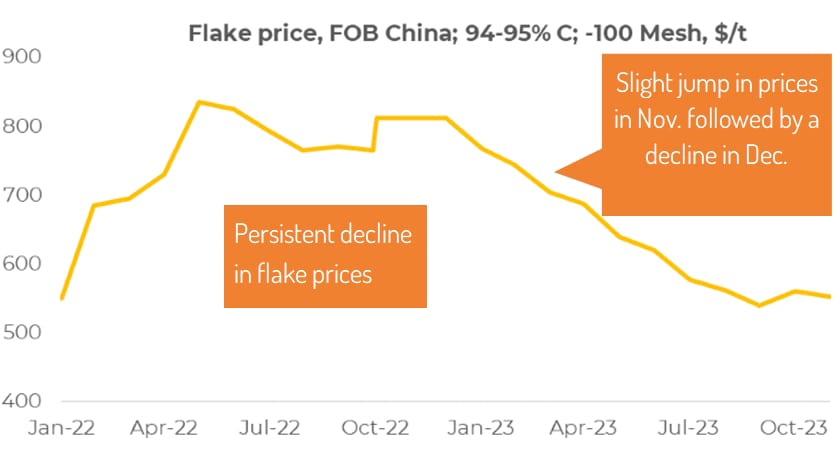

China export legislation temporarily stemmed decline in graphite prices

Export restrictions provided a short-term support to prices in response to stocking ahead of anticipated shortfall in graphite supply. Flake graphite prices increased 4% in November 2023 to $560/t for FOB China; 94-95% C; -100 Mesh following a period of unabated decline since Q2 2022. However, the uptick in prices has proved transient as flake graphite prices fell 1% in December 2023 to reach $553/t.

Source: Benchmark Forecasts

The continued pressure on graphite prices can be attributed to the oversupply across the EV value chain. The global growth in EV sales slowed in 2023 (+30% year-on-year) compared to 60% growth in 2022 on the back of sluggish Chinese economy and removal of EV purchase subsidies in China.

Source: Benchmark Forecasts

South Korea and Japan are most exposed to restrictions, however not most impacted

China controlled over 90% of global anode active material production in 2023 with South Korea and Japan accounting for a mere 7%. South Korea and Japan are most exposed to restrictions as they import all their spherical graphite requirements for battery anode production from China. Reports suggest that China has already issued export permits for spherical graphite to South Korean companies.

Further, a flake and expanded graphite shipment to Germany has also been approved. However, Benchmark understands that approvals have not yet been granted for shipments to India and the US. The comprehensive forms requiring the declaration of end use and other confidential details is discouraging companies to source from China. In addition, the extended timeframe for receiving permits to 30-40 days has added to the time and cost of procuring material from China.

Manufacturers plan decoupling from China through supply diversification

In a bid to diversify supply sources, companies worldwide are exploring alternative sources of graphite supply. As per Benchmark forecasts, Africa is expected to emerge as a leading source for flake graphite supply with around 800kt of new natural graphite capacity being added by 2030. taking the total natural graphite capacity to 2.8mt (vs. 1.2mt in 2023). Countries like Australia, Canada and Brazil are also emerging as reliable sources of flake graphite adding close to 450kt of new capacity.

South Korean anode producer POSCO is a case in point in terms of diversifying supply sources. The company has signed long-term flake graphite procurement agreements with companies in Canada and Tanzania.

Though China is expected to face competition from Australia, North America, and Europe for spherical graphite supply going forward, it is still expected to maintain its dominance controlling more than 50% of global production. China will also continue to dominate the synthetic graphite and active anode material production. The country is adding synthetic graphite production to the tune of 1.3mt and active anode material to the tune of 1.1mt by 2030. Ex-China active anode material capacity additions are expected to be half at close to 500kt.

Government policy designed to support diversification and localised supply chain

To reduce dependence on China or any country for raw material supply, countries are announcing initiatives and policies to boost domestic manufacturing and develop a localised battery supply chain. The US Inflation reduction Act (IRA) and the European Union’s (EU) Critical Raw Materials Act are a case in point.

The US IRA focuses on onshoring (developing domestic capabilities) and friend-shoring via ex-China supply chain diversification. By imposing battery component and raw materials origin requirements, the US IRA aims to support domestic manufacturing.

The US has also imposed Foreign Entity of Concern (FEOC) requirements to be eligible for tax breaks as part of IRA. The guidance was released to the public in December 2023 for comments and considerations before it starts entering into force in 2024. Beginning in 2024, an eligible clean vehicle may not contain any battery components that are manufactured or assembled by a FEOC, and, beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed, or recycled by a FEOC.

Similarly, EU’s Critical Raw Materials Act lays down the limits for materials originating from outside the EU along with benchmarks for processing, recycling, and diversification for materials relevant for the strategic raw materials.

Europe and US are now witnessing new anode capacity additions supported by government policy and a growing realisation that supply chains need to be derisked. Australian company Talga Resources broke ground on Europe’s first anode plant in the north of Sweden in H2 2023. Novonix, Anovion and Syrah Resources, among others, are also building anode projects in the US.

Conclusion

Export controls by China have clearly highlighted the market power and influence the country possesses in the global battery supply chain. Major Governments are aiming to de-risk and decouple from China through legislation promoting domestic manufacturing and limiting dependence. Though projects and investments have been announced in the midstream and upstream battery space, the impact of such initiatives will eventuate overtime. Until then, China will be a dominant producer in global battery supply chains. A co-ordinated and speedy policy and industry response is needed to develop a balanced global battery market.

By Shruti Kashyap

Product Director – Anode, Benchmark Mineral Intelligence.

![]()

Benchmark Minerals specialises in assessing market prices, supply chain data, forecasting and strategic advisory for the technologies and supply chains central to the energy transition. Contact [email protected] for more information.

MMTA Members are entitled to a 15% exclusive discount to all Benchmark Minerals Intelligence Events, including the upcoming Giga Europe 2024 in Stockholm, Sweden on 12-13 March. See MMTA Member Benefits for your discount code.