In this article for The Crucible, Benchmark Mineral Intelligence looks at the market for the secondary battery material mix known as “black mass”, the fundamentals and forecasts that underpin its recently launched Black Mass Price Assessment suite.

Demand for lithium-ion batteries is growing, overwhelmingly being driven by the electrification of transportation. Downstream, cell capacity announcements and expansions continue in a bid to meet OEM demand and EV policy targets, though many bottlenecks lie in the upstream of the supply chain, with Benchmark forecasting deficits across lithium, nickel, and cobalt markets later this decade. Stakeholders from across the supply chain are looking to battery recycling to bolster battery sustainability and circularity credentials, and critically, to help alleviate supply constraints.

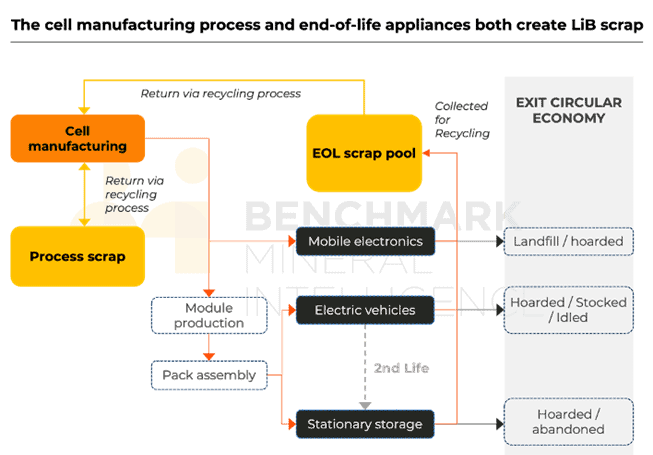

Of course, battery recyclers can only recycle the material that has already been extracted from the ground. That material will ultimately end up making its way into one of two types of recycling feedstock: process scrap and end-of-life (EOL) batteries. Ultimately, rejected material (from process scrap) and EOL batteries must be sorted, discharged, disassembled, and crushed, with the mixture of material produced known as black mass: a critical and valuable intermediate product in the recycling value chain.

Benchmark forecasts that process scrap will be the major source of feedstock for recycling for the coming decade, representing 76% of the global scrap pool today, and 72% in 2030. Across the 2030s, increasing volumes of batteries will reach their end of useful life and retire for recycling.

Benchmark forecasts that process scrap will be the major source of feedstock for recycling for the coming decade, representing 76% of the global scrap pool today, and 72% in 2030. Across the 2030s, increasing volumes of batteries will reach their end of useful life and retire for recycling.

Some may reach this and still have suitable capacity to be redeployed to a second life in stationary storage applications before returning for recycling.

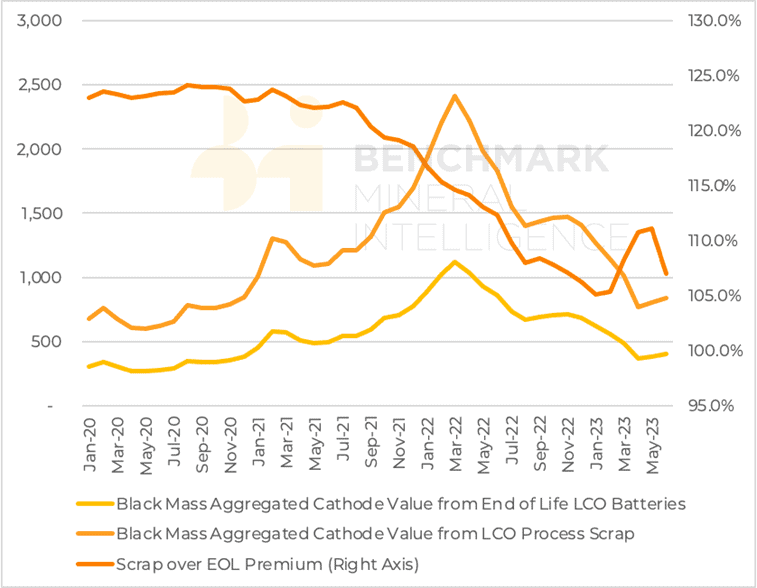

LCO Black Mass – Process Scrap Value vs EOL value ($/t)

The battery market is seeing a wealth of chemistries being deployed across different applications: LCO is particularly favourable for portable applications, whilst high nickel NCM and LFP chemistries have emerged as the leading chemistry variants for transportation. With this, the future pool of material for recyclers will differ year-on-year and region-to-region, necessitating recycling processes to be adaptable and flexible. This diverse pool means that one tonne of black mass is not the same as another, resulting in questions from the industry on the specification of black mass, and if standardisation is possible when it comes to the pricing, trading, and movement of the material.

The battery market is seeing a wealth of chemistries being deployed across different applications: LCO is particularly favourable for portable applications, whilst high nickel NCM and LFP chemistries have emerged as the leading chemistry variants for transportation. With this, the future pool of material for recyclers will differ year-on-year and region-to-region, necessitating recycling processes to be adaptable and flexible. This diverse pool means that one tonne of black mass is not the same as another, resulting in questions from the industry on the specification of black mass, and if standardisation is possible when it comes to the pricing, trading, and movement of the material.

In response to this need, Benchmark Mineral Intelligence launched its Black Mass Price Assessments suite in July, providing the industry with real market trade prices for all of the major specifications trading in China – the current hub of global battery recycling. These price assessments cover payables for lithium, cobalt, and nickel from NCM scrap and EOL feedstocks, and lithium and cobalt from LCO scrap and EOL feedstocks. Additionally, Benchmark uses its proprietary raw material pricing for the virgin market along with these payables to derive an equivalent black mass price for each of those target elements from black mass.

Furthermore, by aggregating these prices, Benchmark publishes a weighted price assessment for black mass from process scrap, and black mass from EOL feedstocks, to give trades a holistic view of the evolving value of black mass across all chemistries.

It is worth noting that pricing of black mass is still reasonably immature. Outside of China, black mass payables are significantly lower and currently only really focus on nickel and cobalt, quoting payables to LME metal prices. However, in a similar way to which the virgin market is moving away from LME metal payables for cobalt and nickel, the black mass market is also looking to more closely align payables to the competing chemical market i.e. nickel sulphate, cobalt sulphate and lithium carbonate. Most payables in China are already quoted on such a basis.

A key challenge for the black mass market to grapple with in the coming years is the lack of standardisation in the black mass itself. By virtue of the wide array of chemistries inputting to the scrap pool – and, of course, the clear difference in the impurity profile and content levels of process scrap versus EOL – traders have so far found the standardisation of black mass specifications to be a significant issue. Black mass from LFP is, therefore, perhaps the easiest black mass product for counterparties to agree a price for; today it is priced purely on a “per percentage point of lithium” basis. Naturally, should the value of retrieved phosphate and iron constituents become a future commercial consideration then black mass from LFP pricing will likely become more complex.

When considering the movement of black mass, there is a current lack of consistent guidance on the rules governing how it is classified and transported around the world. In China, under official guidelines it cannot be directly imported due to it being classified as a toxic material. In the EU, black mass classification is inconsistent which has led the EC to state it will propose the inclusion of waste codes for lithium-ion batteries and black mass under the Europe List of Waste in 2024, seeking to harmonise its guidance. This means black mass would be considered a hazardous waste, requiring permits to transport it across borders.

Beyond the impact of this on transportation procedures, the EC’s decision also endeavours to address concerns of material leakage outside of the region. At present, black mass produced in Europe typically flows towards Southeast Asia for processing – often being processed to mixed hydroxide precipitate (MHP, an intermediate nickel-cobalt product), before going on for further processing to produce battery materials. With targets for battery recycling coming into force in Europe – critically, minimum recycled contents and consumption targets – the bloc sees this loss of material outside of the European battery ecosystem as an obstacle in achieving these targets. Therefore, the goal of preventing this pattern continuing long term could be achieved, in part, by classifying black mass as hazardous.

In tandem with regulatory updates, the recycling industry in Europe is striving to establish increasing hydrometallurgical capacity to process black mass and extract battery materials domestically. Recent announcements such as Fortum Battery Recycling’s hydrometallurgical refining plant in Finland beginning operations in Q2, as well as Li-Cycle and Glencore’s planned joint venture to develop a hydrometallurgical facility at an existing Glencore asset in Italy in the coming years, demonstrate the industry’s efforts to building out capacity within Europe to produce secondary battery materials itself.

By Sarah Colbourn and Daniel Fletcher-Manuel, Benchmark Mineral Intelligence

![]()

Benchmark Mineral Intelligence creates actionable intelligence for the lithium-ion battery to electric vehicle supply chain. Through its services, ranging from price reporting, data, long-term forecasts, consultancy and ESG reporting, Benchmark provides stakeholders with intelligence on all stages of the supply chain.

In response to increasing attention on lithium-ion battery recycling and the black mass market, Benchmark has launched its long-term Recycling Forecast report, and most recently, a monthly Black Mass Price Assessment.

Upcoming Benchmark Mineral Intelligence Events

Battery Gigafactories Asia Pacific 20-21 September 2023, Hilton, Tokyo

Benchmark Week 2023 14-16 November 2023, Los Angeles

MMTA members receive a 15% discount on registration to Benchmark Mineral Intelligence conferences. Find your excusive discount code in the Member Benefits section of this website or your copy of The Crucible magazine.

For all upcoming Benchmark Minerals events, and to register, visit https://www.benchmarkminerals.com/events/