Ferroalloy smelting, by Dushlik, Shutterstock

- FeSi, SiMn quotas nearly exhausted

- Front-loading cushioned Q1 safeguard impact

- Net volumes show structural tightness for Q2

As the first quarter of the EU’s ferroalloys safeguard regime closed on Feb. 17, the European Commission’s quota data showed tightening headroom in ferrosilicon and silicomanganese.

However, market participants described a more nuanced reality: physical pressure in specific pockets, but little evidence of broad-based demand strength.”

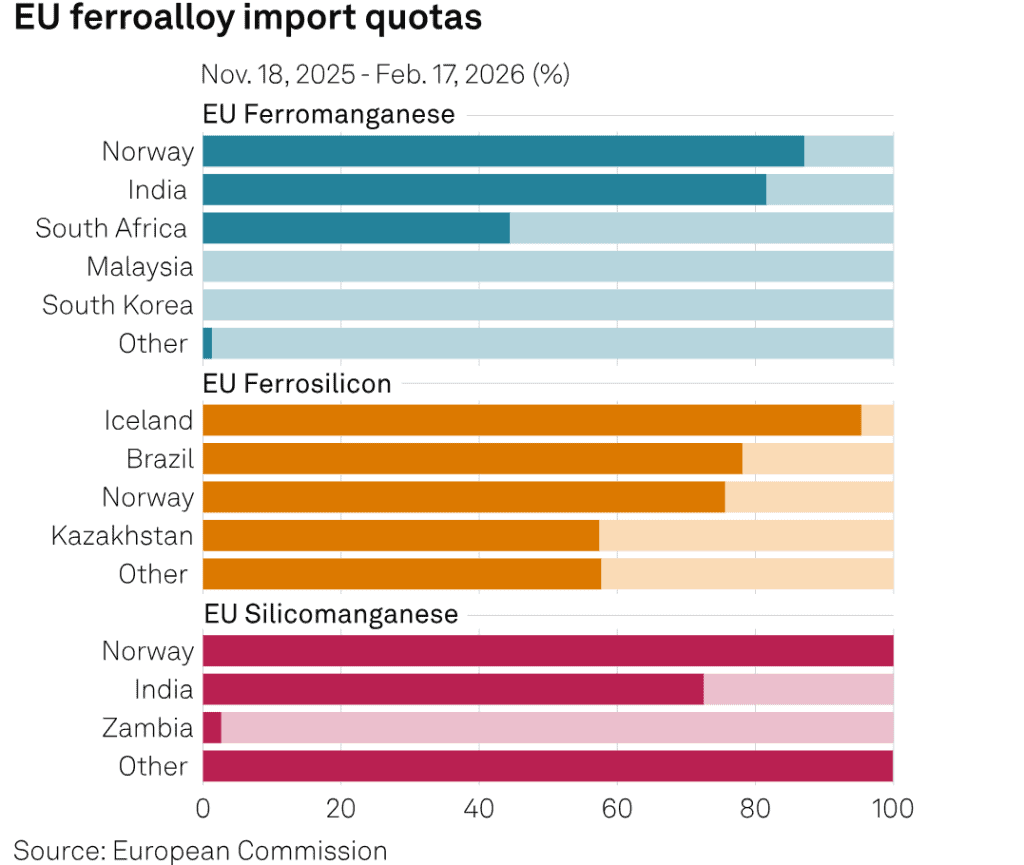

Quarter-end figures showed FeSi with just 15.81% net re-maining once pending allocations were deducted, while SiMn stood at 4.97% net remaining, the most constrained of the four covered products within this legislation.

By contrast, ferromanganese retained 35.37% net remaining, leaving it comparatively insulated from immedi-ate tariff exposure.

Despite the tightening headline numbers, traders said the safeguards have not yet translated into broad price momentum. Demand is simply not there,” a trader said.

“You have the safeguard overlay, but underlying consumption is weak. That’s the bigger driver.”

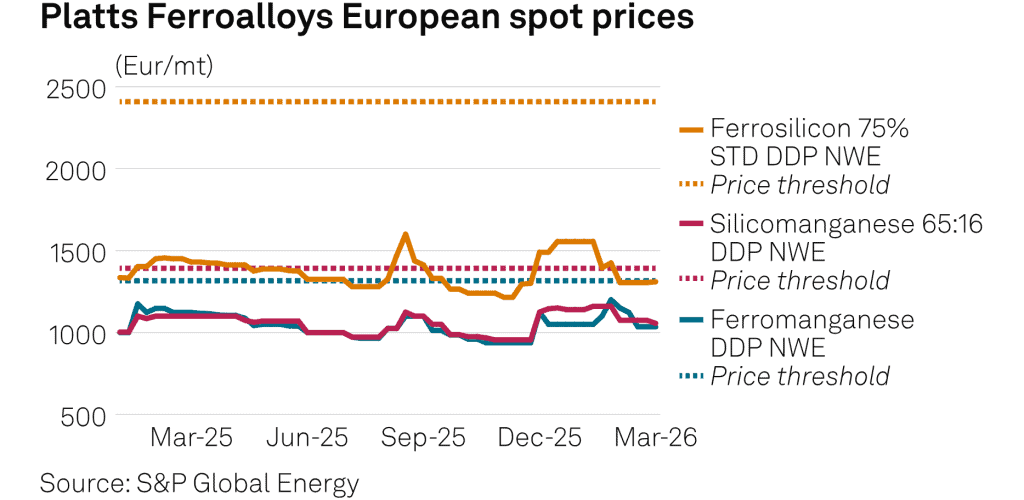

FeMn closed the quarter with more than one third of its quo-ta still available, reflecting both diversified supply and slower offtake. Market participants saw spot indications around Eur1,050/metric ton DDP Northwestern Europe, slightly softer week over week.

Several buyers pointed to heavy front-loading ahead of the Nov. 18 implementation date, which effectively pre-positioned material inside the EU and reduced the need for aggressive Q1 imports.

People put material in before the quotas came into effect,” a second trader said, adding, “stocks were sufficient, so we didn’t feel a squeeze.”

As a result, while the safeguard aims to cap the annualized import allowances at 25% below the 2022-2024 average, the immediate impact on FeMn has been muted by inventory overhang and fragile steel output. SiMn net remaining volume of 4.97% placed it closest to out-of-quota exposure as the second quarter begins. Pending allocations in late Q1 masked how quickly the country-specific buckets were drawn down, with some origins approaching exhaustion in the final days of the quarter.

Yet prices have failed to respond in kind. Spot indications were heard around Eur1,050-1,100/mt DDP NWE, trending downward amid subdued booking interest. “SiMn is going down because the end user demand is weak,” a third trader said.

The quota situation is there, but it’s not pulling prices up.”

Participants cautioned that timing remained critical. With no carryover mechanism between quarters, clustered arrivals early in Q2 could still trigger sudden tariff exposure for specific origins, even if aggregate consumption remains lacklustre.

FeSi imports remained critically close to the quota limit, es-pecially from Iceland. After deducting pending volumes, the alloy entered Q2 with just 15.81% net remaining as of Feb. 18. “There’s no real clarity in the market,” a distributor said. “You have low demand mixed in with tightening country buckets. It’s not adding up to a clear direction.”

Some mills are evaluating silicon metal as a partial substitute, limiting incremental FeSi demand and capping upward price pressure. At the same time, traders expect selective firming in Q2 offers for material linked to constrained origins, partic-ularly if bookings accelerate to secure remaining headroom.

Some in Europe welcomed the ferroalloys safeguards back in November 2025. In its fourth-quarter and full-year 2025 earnings results, Ferroglobe, through its CEO, Marco Levi, outlined a stronger outlook for 2026, with potential gains in market share.

Norway’s Elkem remained more nuanced and neutral, only stating that global trade regulations and protective measures were “likely to continue affecting Elkem’s markets.” In November 2025, the Norwegian company said the safeguards could result in a decrease in sales from their production sites of Rana, Bremanger and Bjølvefossen in Norway, and from Iceland, but would likely be compensated by sales in other European regions.

Elkem reduced capacity at its silicon production sites in Nor-way to “manage inventories,” citing subdued demand for sili-con alloys in Europe. However, Elkem’s earnings declined in Q4 2025.

Recent developments in the Middle East conflict raised concerns among Europe-based buyers about higher costs for imported ferroalloys, but there was no immediate impact on spot prices in Europe as the second quarter began.

By Kamran Jussab

[email protected]

Teo Ngoma

[email protected]