The rare earth industry is entering a more constrained and structurally complex phase, as export controls, pricing mechanisms, and downstream capacity challenges begin to reshape global supply chains. Recent developments suggest that while efforts to diversify supply are accelerating, mean-ingful structural change remains incomplete, particularly in heavy rare earths and magnet manufacturing.

Export Controls Tighten as Japan Enters the Constraint

Export controls on rare earths are no longer a theoretical risk; they are now an embedded feature of the market. China’s April 2025 framework established tighter oversight on dual-use materials, and the January 2026 update extended this by explicitly targeting Japan. While the latest measures do not introduce a new category of restriction, they represent a country-specific escalation, bringing Japan into the same constrained environment previously experienced by US and European defence-linked supply chains.

The inclusion of medium and heavy rare earth elements, along with downstream products such as permanent magnets, has significantly increased regulatory scrutiny. In practice, Japanese companies are now facing stricter licensing requirements, higher compliance burdens, and greater approval uncertainty. More importantly, market feedback suggests that procurement challenges are extending beyond the listed materials, with shipments of non-restricted products also experiencing delays or disruptions.

Japan has since increased drawdown of ex-China supply, particularly for dysprosium (Dy), terbium (Tb), and yttrium (Y).

The result is a sharp contraction in ex-China market liquidity. Japan now competes directly with the US and Europe for a narrow stream of heavy rare earth supply. The global market is therefore shifting from one dominated by China’s abundance to one constrained not just by concentration, but by access and deliverability.

Pricing Signals: Premiums and Floors Reshape Incentives

Market tightening is translating directly into price structures. A clear divergence has emerged between light and heavy rare earths, and between Chinese and ex-China prices.

For heavy rare earths, Dy and Tb premiums are becoming structural, reflecting scarcity and their essential role in high-performance NdFeB (neodymium–iron–boron) magnets. Elevated premiums serve a dual purpose: signalling risk and incentivising new supply. Yet production of HREEs is con-strained by their low geological abundance and complex en-vironmental requirements, limiting rapid response to higher prices. At the same time, structured pricing mechanisms are emerging.

© Benchmark Mineral Intelligence, 2026

The establishment of a $110/kg price floor for NdPr oxide under long-term agreements between Lynas, Japan Australia Rare Earths (JARE), and MP Materials and Depart-ment of War (DoW) marks a shift toward formal pricing benchmarks. Floors provide downside protection to producers and better support long-term planning, while profit-sharing terms maintain exposure to market upside.

However, despite the focus on heavy rare earths, NdPr is ex-pected to remain the primary driver of rare earth basket value. Its dominant share in magnet production means that overall project economics will continue to be heavily influenced by NdPr pricing, even as Dy and Tb premiums shape margins at the high-performance end of the market, and for higher rare earth containing deposits.

Funding and Policy Support: Necessary but Not Sufficient

Governments are stepping up direct involvement in rare earth supply chains, led by Japan and the US. Policies now combine funding, stockpiling, and procurement mandates. The US National Defense Authorization Act, for instance, will prohibit the federal purchase of Chinese-processed rare earth materials from 2027.

In parallel, DoW has committed approximately $1.37 billion across 2025–2026 to support upstream and midstream de-velopment, alongside long-term agreements with Lynas and MP Materials.

However, physical diversification alone, adding new mines and refineries, may not achieve full structural resilience. The current system still lacks diversified pricing frameworks and transparent market infrastructure. Many projects therefore remain exposed to China-driven market dynamics, particularly given the absence of reference benchmarks or futures instruments.

Long-term offtake agreements, such as those seen with JARE and MP Materials, are therefore emerging as critical tools. These agreements not only provide revenue certainty but also help de-risk projects in a market where spot pricing is volatile and opaque. However, broader adoption of such structures is still limited.

Looking ahead, there is a growing recognition that the industry may require more sophisticated market infrastructure, including transparent pricing benchmarks and potentially even forward or futures markets, to support investment at scale. Without these, structural exposure to China-driven pricing dynamics is likely to persist.

Magnet Capacity: The Emerging Bottleneck

© Benchmark Mineral Intelligence, 2026

As investment expands upstream, attention is turning to the downstream magnet sector, now positioned as the next major constraint.

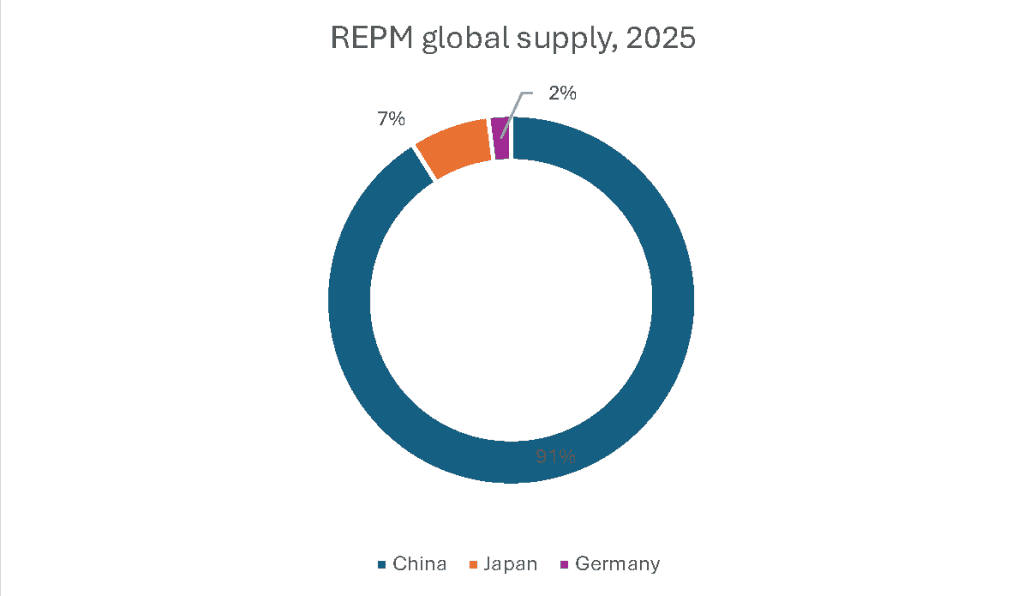

China retains overwhelming dominance in magnet manufacturing, supported by integrated feedstock supply, technical expertise, and economies of scale. Yet Japan occupies a strategically pivotal position in the high-performance segment. Companies such as Proterial, Shin-Etsu Chemical, and TDK have long led in advanced NdFeB magnet technology, including grain boundary diffusion and high-coercivity designs.

These capabilities support critical applications in EV traction motors and precision electronics. This technological edge, how-ever, exposes Japan to upstream vulnerability. Restricted access to Dy and Tb complicates production of high-temperature magnets, while alternative sources remain limited.

Efforts to build ex-China and ex-Japan magnet capacity are proceeding but remain early stage. High-performance magnet manufacture demands tight control over microstructure and efficient utilisation of scarce inputs, requiring substantial know-how and process IP. Barriers to entry are therefore high.

Even if upstream mining and separation expand successfully, the scarcity of downstream processing and magnet manu-facturing capacity could limit supply diversification at the functional end of the value chain. Sustained investment in technology transfer and end-use production is thus as critical as developing raw material sources.

© Benchmark Mineral Intelligence, 2026

Recycling: Opportunity and Constraint

Recycling offers a long-term opportunity to supplement primary supply, mitigate environmental pressures, and enhance resource efficiency. However, its near-term contribution will be modest. The current supply of end-of-life magnets, par-ticularly from EVs and wind turbines, remains low. Material recovery processes require complex dismantling, separation, and refining stages, often yielding variable quality. Maintaining consistent performance, especially for high-grade magnetic alloys, is challenging due to contamination and microstructural degradation.

As a result, recycling is best viewed as a stabilising complement rather than a capacity substitute. Over time, as scrap volumes rise and recovery efficiency improves, recycled feedstock will become a more material factor—but it will not remove dependence on primary mining in the 2020s.

Demand Outlook and Industry Trajectory

Despite tight supply, demand for rare earth magnets continues to expand, driven by EVs, renewable energy, and elec-tronics. The compound annual growth rate of NdFeB magnet demand remains positive across all regions. However, an im-portant shift is unfolding: the drive to reduce exposure to heavy rare earths.

Automotive and industrial manufacturers are pursuing strategies to lower Dy and Tb intensity. Advances in grain boundary diffusion allow reduced Dy loading without compromising coercivity. In parallel, OEMs are investing in magnet-free motor designs—such as induction and switched reluctance systems—and improving material efficiency through microstructural optimisation.

These innovations will not eliminate heavy rare earth use but will moderate demand growth. HREEs will remain essential in applications requiring thermal stability and high coercivity, particularly for high-speed EV traction motors and offshore wind generators. The net effect will likely be a gradual decline in HREE intensity per unit of magnet, offset by continued ex-pansion in total magnet volumes.

The result is a nuanced market trajectory: persistent tightness in heavy rare earths, healthy demand growth for NdPr-based materials, and structurally elevated strategic value for high-performance magnet inputs.

Conclusion

The rare earth sector is moving into a new structural phase marked by constraint, complexity, and strategic sensitivity. Export controls are tightening, liquidity outside China is shrinking, and Ex China downstream magnet capacity has emerged as a defining bottleneck. Government support and private investment have strengthened Ex China supply growth, but the system remains incomplete. Heavy rare earth supply is limited, recycling is immature, and market transpar-ency is underdeveloped.

The industry’s next phase will depend on building interconnected, technologically advanced, and structurally independ-ent value chains that span mining to magnet manufacturing. Until that integration is achieved, rare earths will remain not only a foundation of the clean energy economy, but also one of its most strategically exposed links.

By Neha Mukherjee

Research Manager – Rare Earths

Benchmark Mineral Intelligence

Charts:

- REO — Rare Earth Oxide (REO equivalent in rare earth imports)

- REPM — Rare Earth Permanent Magnets