Cobalt has rallied in price since the Democratic Republic of Congo (DRC) imposed an export ban and introduced a quota system, which has excited traders but concerned consumers. However, sourcing cobalt from elsewhere presents challenges, as Fastmarkets explores.

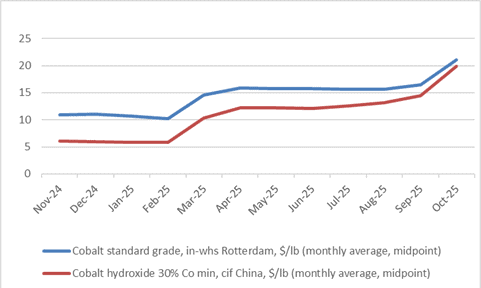

Cobalt metal prices have more than doubled since the start of the year.

Cobalt metal prices have more than doubled since the start of the year.

On Friday November 7, the average of Fastmarkets’ daily price assessment for standard grade cobalt,

in-warehouse Rotterdam, was $23.53 per lb. This is up from $9.95 per lb on February 20, before the DRC put an export ban in place. The DRC banned cobalt exports in February-October to rebalance an oversupplied market, as the government stated and followed up with introducing a quota system from October.

The DRC is the world’s largest source of cobalt, with mined production also from Indonesia, Canada, Norway, Philippines, Russia, Australia and Madagascar. Recycled supply is also a developing source of secondary supply. Could the non-DRC options be enough to replace the missing volumes from the export quota system?

Recycled cobalt: demand is growing

In October, the appetite was high for black mass, a cobalt-containing intermediate in the battery recycling process.

Payables went up for black mass with lithium cobalt oxide (LCO) and nickel-cobalt-manganese (NCM) chemistries.

Payables mean the proportion that consumers pay of a benchmark price for a commodity — in this case, the low end of the Fastmarkets’ price index for standard grade cobalt.

In mid-October, the payables for the high-cobalt LCO black mass reached new historical highs, up to 80%. Demand flowed from Asia, which is the main processing hub for battery recycling.

In terms of volumes, Fastmarkets expects recycled cobalt production to reach approximately 31,000 tonnes in 2025 globally. This recycling volume makes up 12% of the total refined cobalt production across the world, which

Fastmarkets estimates would reach 266,000 tonnes this year. The other 88% should still come from mined supply.

Asian supply: Indonesia leads the way

Indonesia has been emerging as a notable supplier of cobalt, mainly as a byproduct of nickel production. Cobalt is sourced from mixed hydroxide precipitate (MHP) and nickel matte (a feedstock for nickel metal or for battery-grade

nickel sulfate). Prices for MHP have also climbed recently.

Fastmarkets’ cobalt mixed hydroxide precipitate payable indicator, cif China, Japan, and South Korea has increased from 73% (to cobalt metal standard grade in-whs Rotterdam) on October 1 to 90-95% in early November.

This is a record high since Fastmarkets started to track the price in October 2023.

“Previously, when selling high-grade nickel matte, the cobalt contained in it was given away for free,” a nickel matte supplier told Fastmarkets. Now, the market has started pricing the cobalt content with nickel matte, the source added.

Indonesia produced 28,010 tonnes of mined cobalt and 8,160 tonnes of refined cobalt in 2024, Fastmarkets’ analysts say. The gap between mined and refined production reflects the fact that most Indonesian MHP production is exported to

China for refining.

“With low nickel prices, nickel is essentially the byproduct of cobalt production in Indonesia,” another market source joked, when talking to Fastmarkets.

Indonesia was the world’s second-largest producer in 2024, with 10% of the market. The main metal supplier is China-incorporated Lygend. And Fastmarkets’ analysts expect Indonesia’s refined production to more than double over the next decade.

Apart from Indonesia, cobalt in Asia can be mined in Philippines. Cobalt from Japan’s Sumitomo Metal Mining’s (SMM) could be sourced from its Philippines nickel-cobalt operations. SMM’s total global cobalt output for 2024 and 2025 has been approximately 5,000 tonnes per year.

Europe: cobalt production stable, declining or untouchable

In Europe, cobalt can be found in nickel-cobalt mines in Norway or Russia, but supply has been either

decreasing or is not available to the European market.

Swiss-headquartered Glencore operates nickel-cobalt facilities In Norway. Glencore does not publish statistics by country, but its production of cobalt metal from its operations in Norway and Canada was 2,000 tonnes in nine months of 2025 — down by 13% year on year.

Some material, which comes from Europe, is off limits to Western consumers. Russia is under several sets of Western sanctions in response to its continuing invasion of Ukraine that began in 2022.

In October, Russia-based nickel-cobalt producer Nornickel announced it planned to restart production from its Kola plant, which was damaged by fire in 2022. The planned capacity is 3,000 tonnes of cobalt metal per year.

The company is not directly sanctioned, but some Western consumers have said they would not accept Russian cobalt.

“We cannot do anything with this material, and we haven’t been in touch with the company recently,” a US-based trader told Fastmarkets.

Americas and Australia: cobalt output varies

In the Americas, cobalt can be mined in Canada and in Cuba. As well as Glencore, Brazil-based Vale Base Metals also operates nickel-cobalt mines in Canada. Vale produced roughly 2,000 tonnes of cobalt metal in 2024, with a similar guidance published for 2025.

A Canada-headquartered company, Sherritt Internatioal oversees nickel-cobalt operations in Cuba. Sherritt produced approximately 3,206 tonnes of finished cobalt in 2024. In October, Sherritt decreased annual 2025 output guidance to 2,700-2,800 tonnes, due to the impact of Hurricane Melissa and lower-than-expected feed availability. Additionally, US consumers can’t work with Cuban material due to the trade embargo imposed in 1962.

And in Glencore’s Murrin Murrin facility in Australia, the only operating cobalt producer in the country, output was 1,900 tonnes of metal for the first nine months of 2025, including third-party feed, down by 14% year on year after maintenance downtime.

Overall, guidance indicates supply from production sites, such as Sherritt’s, Glencore’s Murrin Murrin or Ambatovy’s

mine in Madagascar has fallen. This reduces the availability of non-Chinese metal on the cobalt market.

DRC: the lion’s share

Apart from the DRC, cobalt in Africa can be sourced from Madagascar and Morocco.

Ambatovy, owned by Sumitomo Corporation of Japan and KOMIR of South Korea, produced 2,535 tons of cobalt metal in Madagascar in 2024. And in Morocco, CTT produced 1,286 tonnes of cobalt in 2024, the company said.

However, the DRC’s mined cobalt production is expected to reach 208,000 tonnes in 2025, according to Fastmarkets’ analysts. Output from DRC copper-cobalt operations vastly exceeds production from the rest of the world.

In 2024, the DRC provided 78% of the global market share of mined cobalt. The top three DRC producers are China’s CMOC, Glencore and Luxembourg-headquartered Eurasian Resources Group.

Lack of alternative to the DRC

Nickel and copper markets have been driving the cobalt supply outlook, according to Olivier Masson, principal analyst at Fastmarkets. Outside of the DRC and Indonesia with 10%, the rest ofAfrica, the Americas, Australia, Europe (including Russia), accounted for less than 3% each in 2024.

Cobalt is a by-product of copper mining in the DRC. And cobalt exports from the huge Central African country have been restrained by export quotas. Meanwhile, supply from outside of the DRC tends to be linked to the nickel market, which has been depressed and oversupplied since 2022.

“The additional supply from new MHP capacity in Indonesia will not be sufficient to offset the loss of supply from the DRC,” Masson said. “And with the nickel prices at low levels, any investment in supply beyond the already under-construction capacity is unlikely in the near-term.”

By Sofia Okun

Price reporter, Fastmarkets