Nickel ore being loaded on South Sulawesi, Indonesia, rdp collection, Shutterstock

Balancing Indonesian Dominance, Shifting Demand, and Policy Uncertainty

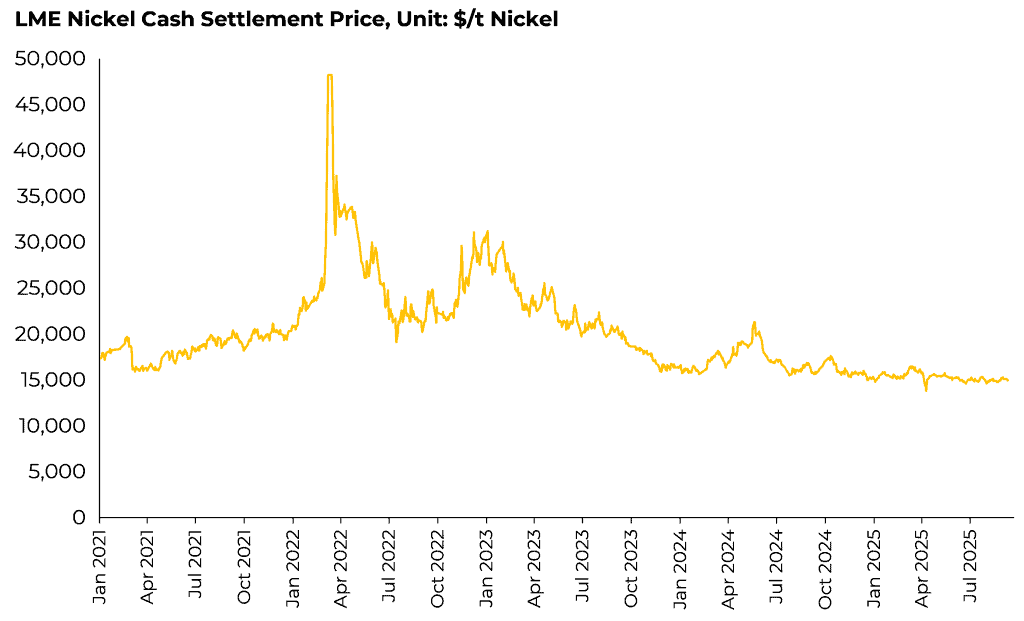

The nickel market is now entering its fourth consecutive year of oversupply. Prices that just three years ago spiked above $25,000/t, and even briefly surged during the 2022 short squeeze above $100,000/t intraday, have since retreated to trade mostly between $15,000–15,500/t in 2025, with more recent levels dipping into the $14,000/t territory. These sustained low prices are the result of a market in surplus due to lower-than-expected nickel demand compounded by a supply wave from Indonesia that has reshaped the structure of the global market.

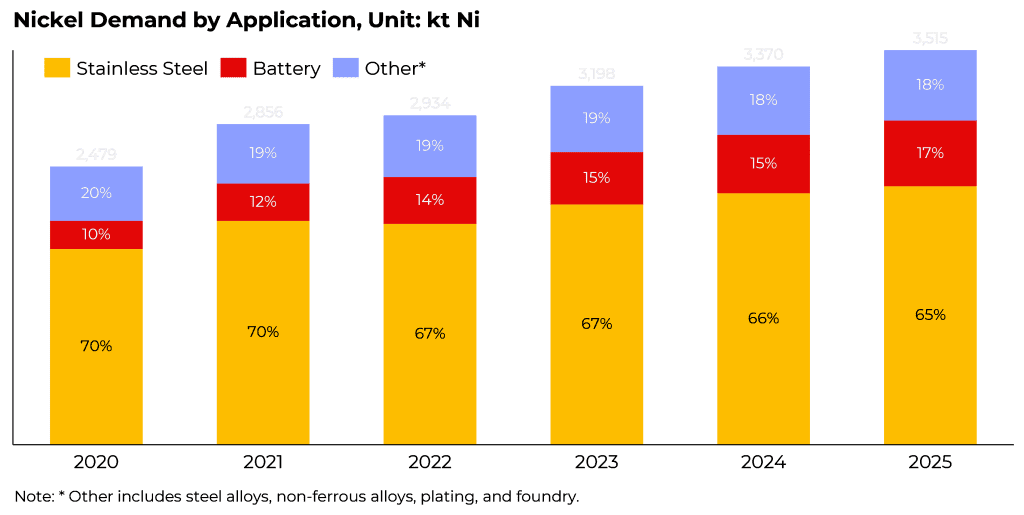

On the demand side, stainless steel continues to dominate nickel consumption, accounting for roughly two‑thirds of the total demand. Growth in stainless has slowed in recent years, weighed down by trade frictions, inflation, tariffs, and weaker macroeconomic conditions in key economies. Lithium-ion battery (LiB) demand, which represents the second largest end-use of nickel at approximately 17% in 2025, is also being reshaped by shifts in battery technology.

Lithium iron phosphate (LFP) cathodes, which contain no nickel, have gained a large share of the LiB market, particularly in China, thanks to lower costs, better thermal stability, and improved performance for shorter‑range vehicles. This has reduced nickel’s share of the cathode mix compared with earlier expectations. Despite this, nickel‑rich chemistries, such as nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium (NCA), remain essential for medium‑ and high‑performance electric vehicles (EVs), which underpin demand in Europe and North America.

Indonesia’s Emergence

Indonesia’s Emergence

The much larger story, however, lies on the supply side. Indonesia has transformed the global nickel industry. A decade ago, Indonesia accounted for only 2% of global refined output. By 2025, its share exceeds 60% – a transformation unmatched in the history of the nickel industry. The turning point was the government’s 2020 ban on raw ore exports, which forced Chinese stainless producers to invest directly in processing capacity within the country. This sparked an extraordinary build‑out of smelters, refineries, and processing plants, concentrated in vertically integrated industrial parks such as Indonesia Morowali Industrial Park (IMIP) and Indonesia Weda Bay Industrial Park (IWIP).

These industrial hubs, managed and largely financed by Tsingshan, the largest stainless steel and nickel pig iron (NPI) producer in the world, as well as other Chinese firms, ensure access to captive laterite ore mines, integrated power plants, sulphuric acid facilities, and a skilled workforce in one location. This scale and integration have given Indonesian producers a structural cost advantage, allowing for efficient procurement of raw materials and economies of scale in processing.

These industrial hubs, managed and largely financed by Tsingshan, the largest stainless steel and nickel pig iron (NPI) producer in the world, as well as other Chinese firms, ensure access to captive laterite ore mines, integrated power plants, sulphuric acid facilities, and a skilled workforce in one location. This scale and integration have given Indonesian producers a structural cost advantage, allowing for efficient procurement of raw materials and economies of scale in processing.

Critically, the Indonesian nickel supply chain is becoming more dynamic and flexible, adding options to produce different products for different markets. This flexibility has become central to Indonesia’s role in the market. Traditionally, nickel was segmented into Class 1 (refined nickel metal with purity >99.8%) and Class 2 (NPI and ferronickel, which have nickel content lower than 99.8%).

Today, the line between them is increasingly blurred. Indonesian producers can pivot material destined for the stainless or battery markets depending on relative prices and payables. This has eroded the traditional Class 1 vs Class 2 distinction, meaning oversupply in one segment spills more quickly into the other. By contrast, most non‑integrated smelters outside Indonesia lack this optionality, making them unable to take advantage of arbitrage opportunities.

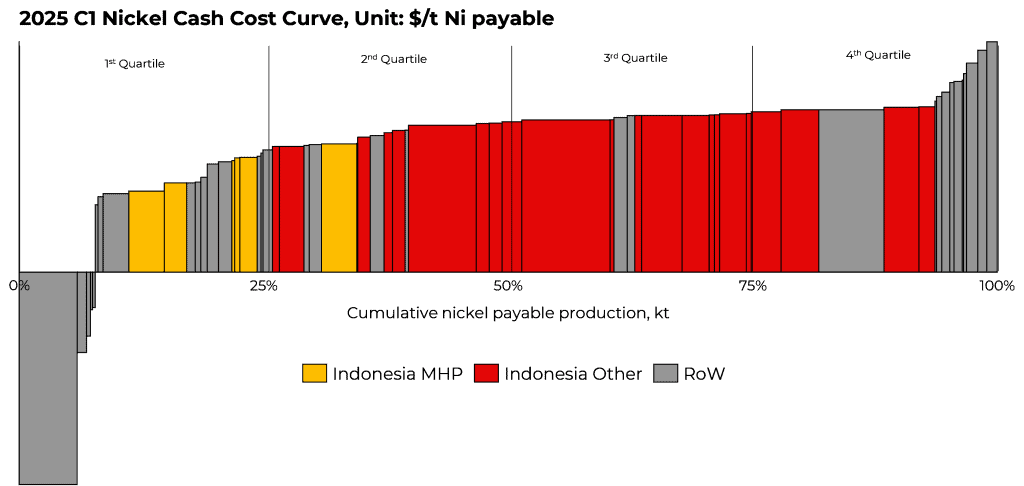

According to Benchmark Mineral Intelligence’s nickel cost model, Indonesia maintains one of the lowest average cost positions globally at around $13,500/t Ni payable. Within that, integrated HPAL facilities producing MHP have the lowest C1 average cash costs at ~$9,800/t Ni payable, benefitting from cobalt by‑product credits. Meanwhile, NPI and nickel matte operations in the country have higher industry cash costs, averaging close to $14,700/t and $15,100/t, respectively – therefore, at current prices, they are seeing their margins squeezed, with some losing cash.

Outside of Indonesia, many traditional producers have faced mounting pressure. In Australia, eight nickel operations were active in 2022 producing 154kt Ni (5% of global mined supply). By late 2025, only two remain: IGO’s Nova and Glencore’s Murrin Murrin, together supplying just a fraction of former domestic output (51kt Ni, accounting for 1.3% of global mined supply). Nova is nearing the end of its mine life next year, meaning Glencore will be the only nickel operator left in Australia, traditionally a major nickel player. Similar pressures are being felt in New Caledonia, as well as for Chinese NPI producers and mature ferronickel smelters in Asia (excluding Indonesia), with average costs of these operations trending above $15,500/t. However, some of these high-cost operations are expected to endure the low-price environment as they remain socially and economically important for employment and revenues even as their cost positions are challenged on the global curve.

Indonesian Policy Risks Shape the Path Ahead

Indonesian Policy Risks Shape the Path Ahead

Despite its dominance, the pace of Indonesia’s growth is not guaranteed. The most important factor that will determine the market direction is Indonesian government policy. There are several measures that the government has implemented and is planning to implement that signal a shift from the previous exponential growth that Indonesia has achieved.

The enforcement of tighter nickel ore quotas (RKAB), which are currently issued on a three‑year basis, but have been renewed to be given annually, demonstrates the state wants greater control over production volumes.

Between 2023 and 2025, delays in RKAB approvals have caused bottlenecks and left some smelters short of ore, lifting premiums for saprolite supply. At the same time, saprolite ore quality is in decline, with average grades falling. Producers are increasingly turning to imports from the Philippines to compensate, introducing fresh exposure to Philippine export policies and weather‑related supply disruptions.

Royalties have also shifted. For saprolite ore used in NPI production, rates rose from a flat 10% to a sliding 14–19%, linked to international nickel prices. By contrast, limonite ore, the primary feedstock for MHP, nickel sulphate and the broader EV battery supply chain, is subject to a royalty of just 2%. This structure effectively channels investment toward the battery industry, emphasising the government’s downstreaming strategy.

Tighter scrutiny has also been applied to HPAL project approvals. Environmental permitting has become more demanding, with a focus on tailings containment and long‑term storage solutions. Projects not aligned to international standards could face delays in commissioning. At the same time, crackdowns on illegal mining operations in forests demonstrate the government’s willingness to intervene both on regulatory and environmental grounds.

Together, these measures underline the central role of Indonesian government decisions in shaping global nickel supply. While production will continue to grow, these measures pose a risk to the outlook. Approvals, ore quality, and ESG compliance will be decisive in determining how much new nickel enters the market, and at what pace.

What’s next for the nickel market?

The central narrative for the nickel market is clear. Robust but evolving demand growth is colliding with a supply base dominated by one country, where costs are low, reserves are vast, and integration enables switching between product types. The downside is that the entire system is now more exposed than ever to the direction of Indonesian government policy.

Western producers will continue to struggle where costs are unsustainable, with only a handful of integrated or strategically important operations likely to survive. In higher‑cost jurisdictions such as Canada, Australia, and New Caledonia, survival may increasingly depend on state support or recognition of local economic importance.

For Indonesia, the next phase will see competition intensify within its own borders. Producers that combine full vertical integration across upstream and downstream with higher ESG standards will be best positioned to secure access to premium US and EU markets. At the same time, higher ESG compliance requirements may raise operating costs across the board, slightly narrowing the competitive gap with other jurisdictions.

The cost curve further highlights this fragility. Integrated industrial parks cluster around similar costs, creating a flat level through the middle of the curve. As a result, even a modest price decline can push a large portion of supply into cash‑negative territory, forcing some operations to exit the market. Such supply rationalisation has the potential to tighten balances and lift prices, but the pace and extent of this adjustment will be shaped by Indonesian government policy and the acceptance of its material in the energy transition supply chain.

For further insights on nickel or other critical minerals, go to www.benchmarkminerals.com

By Jorge Uzcategui

Principal Analyst – Nickel & Cobalt

Benchmark Mineral Intelligence