- Molybdenum oxide prices surged after mining

accidents in China, Chile - Asian demand for moly products remained robust

- Impact from tariffs remains limited on oxide

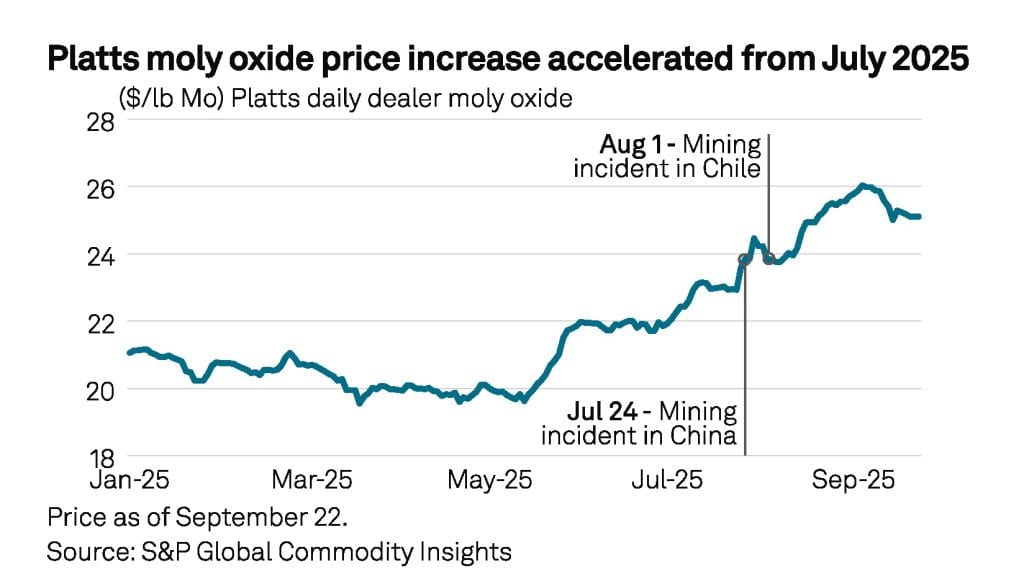

Molybdenum oxide powder spot prices have surged to their highest level this year, climbing from July as molybdenite concentrate supply continued to tighten.

Platts assessed spot prices at $26.025/lb Mo on 3 Sept, up from $21.925/lb Mo on July 1, a price level last seen on Aug. 11, 2023, according to S&P Global Commodity Insights. Prices have since eased slightly to $25.05/lb Mo on Sept. 24.

Market sources struggled, at the start of 2025, to anticipate future price movements because of uncertainties surrounding global trade policies from the US, fluctuating demand levels, and the economic outlook in Europe. Prices were rangebound until May when supply tightened and China’s demand firmed.

Robust Chinese demand for moly oxide powder came while concentrate supply remained stable with prices subsequently increasing close to Yuan 4,000/mt (about $562.42/mt).

Mining incidents cause supply tightness

On July 24, 2025, a fatal incident where six people died while visiting a dressing plant copper-molybdenum mining site owned by Zhongjin Gold Corp in Inner-Mongolia, China, prompted a production suspension.

Although the incident had no significant impact on the copper spot market, the news triggered a price hike in molybdenite concentrates in China, leading to a subsequent increase in oxide powder spot prices. Such an increase came at a time of precarious equilibrium on the market, due to high levels of enquiries for moly concentrates, and production lagging behind demand, leaving prices more volatile.

Platts Moly Oxide Daily Dealer gained $0.675/lb Mo day-over-day on July 24, and peaked at $24.45/lb Mo on July 29,

Platts Moly Oxide Daily Dealer gained $0.675/lb Mo day-over-day on July 24, and peaked at $24.45/lb Mo on July 29,

following the incident.

“The Chinese market relies a lot on Chinese domestic products of concentrates,” a second trader said. “This kind of news always triggers a reaction from the Chinese market.”

A week later, a 4.2-magnitude earthquake caused a tunnel collapse at Codelco’s El Teniente copper mine in Chile, killing six workers, and halting production to allow rescue teams to carry out a search. On Aug. 4, Chile’s mining minster Aurora Williams declared in a press conference El Teniente was operating at 10% capacity. However, the accident did not produce the same supply shock as the July 24 accident.

Market participants said that while the short-term impact of reduced production at El Teniente was challenging to quantify, the delicate balance between demand and supply left the global molybdenum market vulnerable to price increases. Demand for moly products, including oxide powder and concentrates, remained robust in Asia, particularly in China.

On Sept. 2, Codelco announced it managed to resume operations at El Teniente mine at 60% of its usual capacity. The overall economic impact was estimated at $340 million.

From Aug. 1 to Aug. 11, the Platts Daily Dealer Moly Oxide price remained stable before rising to $24.925/lb Mo on Aug. 14, a surge attributed more to the dynamic nature of the Chinese market than to the fallout from the Chilean mining incident.

Tariffs update

US trade policy under the new Trump administration largely dictated 2025 economic news, with higher trade tariffs on US imports. Following the US announcement of additional tariffs on April 2, several trade agreements were announced between different trading partners including Vietnam, Japan, South Korea, and the European Union, setting the stage for higher import prices on numerous products to the US.

Molybdenum, not on the list of exempted products as of September 2025, faces an ad-valorem tariff of 10%. Although the US could rely on domestic molybdenum production, tariffs affected the ferromolybdenum spot market, more reliant on imports, rather than the moly oxide market.

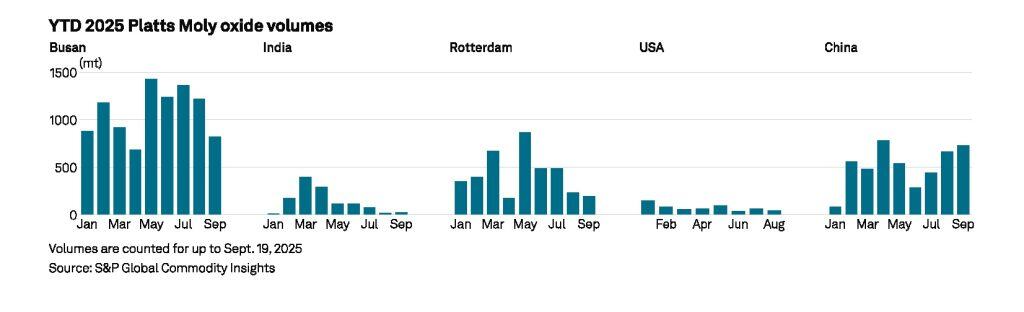

The US administration announced additional 25% tariffs on Indian exports to the US on July 30, causing turmoil in the Indian steel market and prompting a bearish outlook from market participants.

“The market has been quiet since the tariffs announcement,” a third trader said.

Current oxide powder prices have pressured Indian end-consumers to enter the spot market and cover their supply needs, but some buyers also adopted a wait-and-see stance while gauging the direction of India-US trade negotiations.

Typically, the Indian molybdenum market trades at a premium of approximately 20 cents/lb over Busan, Tianjin, or Rotterdam material. Following the July 30 announcement, traded volumes reported to Platts on the Indian spot market plummeted from 75 mt in July to only 15 mt in August.

Price softening and Q4 outlook

Price softening and Q4 outlook

Since the start of September 2025, prices began to correct as market participants anticipated lower prices when the dressing plant owned by Zhongjin Gold Corp restarts production, would likely trigger softer prices on oxide powder. In addition, market sources who participated at an industry event in Chile in September suggested that market fundamentals were not expected to drastically change in Q4 2025.

They noted that Asian demand for oxide powder and concentrates would remain strong through the first quarter of 2026, citing a lack of new mining projects approved in China and increasingly stringent environmental regulations affecting the Chinese mining sector.

They noted that Asian demand for oxide powder and concentrates would remain strong through the first quarter of 2026, citing a lack of new mining projects approved in China and increasingly stringent environmental regulations affecting the Chinese mining sector.

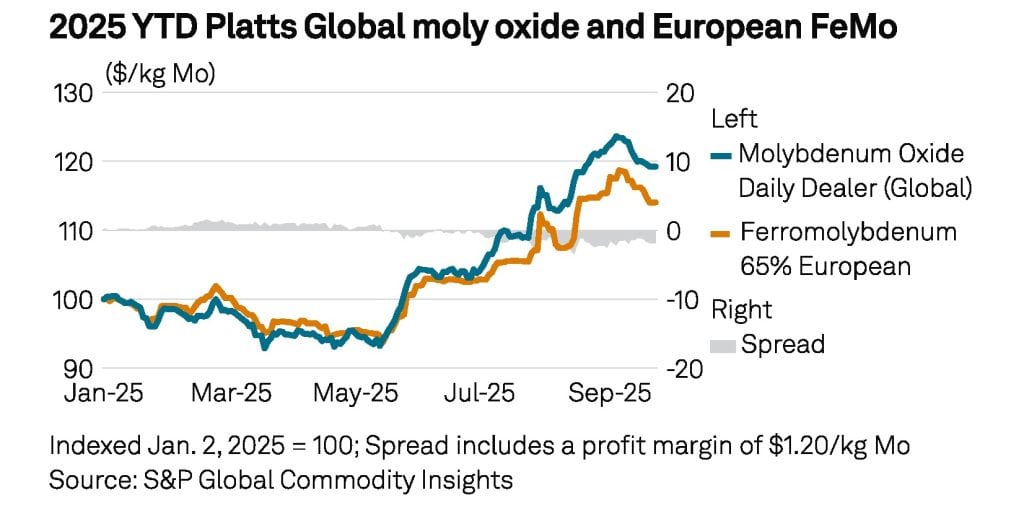

European demand, which had been sluggish in July and August due to the seasonal summer slowdown, continued to lag in September 2025, with minimal spot activity reported to Platts since September 1 in the molybdenum oxide and

ferromolybdenum markets.

“The discrepancy between oxide and FeMo prices is not a good sign for the European economy,” a fourth trader said.

On Sept. 19, Platts assessed the European price for ferromolybdenum 65% at $57.25/kg Mo. The spread between the estimated conversion cost from oxide powder and the European spot assessment for the ferroalloy remained negative on Sept. 19 at -$1.84/kg Mo.

By Teo Ngoma

Price Reporter